Nothing “Semi” About the Semis…

“Semi” is a Latin-derived prefix meaning half, partly, or incompletely. There is very little about the semiconductor business that is half, part, or incomplete right now. As discussed in last weekend’s Moonshot, the chip sector continues to drive markets. While NVDA dropped over 8% from an all-time closing high on Monday, the SOXX ETF (a semiconductor ETF) finished the week at its all-time closing high.

- SOXL, a 3X leveraged semiconductor ETF, hit a record with $17 billion in total assets (despite seeing shares outstanding decline as some investors took profits). We are having a lot, and I mean a lot, of conversations about market structure. It is difficult to underestimate the power of leveraged ETFs and their ability to make daily swings even larger than they “should” be. The daily rebalancing is impactful, especially when we are getting relatively large daily moves.

- INTC (which we have as part of our ProSec™ theme) was up 20% on the week, barely outpacing gains from QCOM. While not in the semiconductor space per se, NOK is a name we have discussed as part of European ProSec™, and it is up 35% in the past 7 trading days!

It seems that:

- The market has decided that it is easier to bet on the semiconductor industry than it is to bet on “big tech” more broadly. Yes, the Nasdaq 100 is at an all-time high (aided by a healthy dose of semiconductors), but it has underperformed. Have investors decided it is “safer” to bet on the chips, rather than who will benefit most from their use of chips?

- As discussed above, the last move higher in semis came without the leadership of NVDA. Does the fact that NVDA can fall 8% (but the sector can rally) indicate that companies seem to be willing to bet on others developing AI-suitable chip technology? Other devices being used to access the AI product and the corresponding needs for those devices? The market may be spreading its bets around other makers, as companies are competing to deliver AI more efficiently.

These trades have been playing out from time to time, but it seemed to solidify into an investment theme last week that is difficult to ignore.

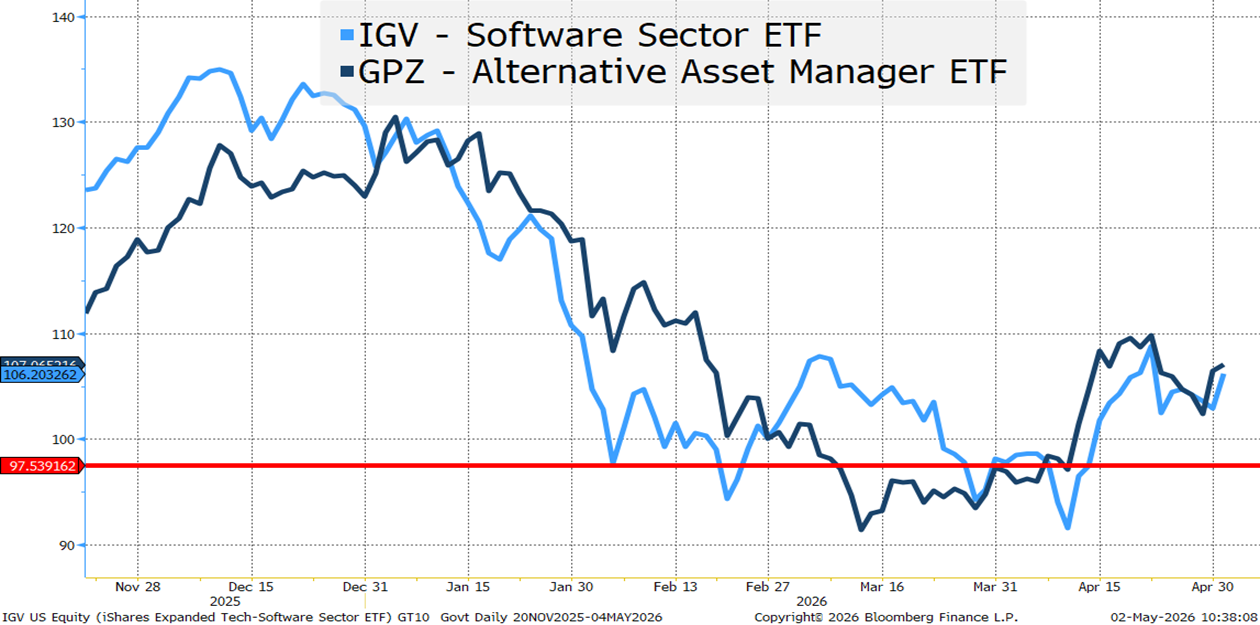

I find this chart “curious” in one way, and “telling” in another.

The “curious” part is that if you would have told me this time last year, that trading software stocks and trading the stocks of alternative asset managers was the same thing, I likely would have scoffed at that. Yet here we are. If I would have scoffed at this once, why should I accept the pattern today?

- Private Credit has exposure to loans to software companies.

- Alternative Asset managers have exposure to private credit.

Sure, I get that, but….

- The 5 largest holdings in IGV (the ETF above) are ORCL, MSFT, PLTR, CRM, and PANW.

- The 5 largest holdings in GPZ (the ETF above) are BX, BN, KKR, APO, and BAM (BN and BAM are listed in Canada).

I think the correlation should break.

- I like the alternative asset managers here. We first started nibbling a few weeks ago, but I am liking them more as I believe the damage associated with private credit is overdone (at least for now). One thing I don’t hear much about is that it is completely logical that if you had an opportunity to get out at par on something you believe may not truly reflect value AND you had the opportunity to put that money right back into private credit in vehicles that did reflect that value, you would be remiss not to. If I can take my money out of vehicle A at 100 and buy vehicle B, with a similar collection of assets, at 80, why wouldn’t I do that? People treating the redemption requests as investors fleeing private credit probably created the “wrong” impression. Yes, some people were pulling out, but many others were looking to take advantage of the disconnect between vehicles A and B. I think the trend in redemption requests will diminish far more rapidly than the market currently seems to be pricing in, as the markdown of loans continues to highlight the disconnect between vehicles.

- This is where I confuse myself.

- As a contrarian I want to play for a big bounce in software. But this ETF hasn’t even gotten back to levels from just a couple of weeks ago. Not very encouraging, even as a contrarian.

- My bigger concern is that this investment theme of betting on chips and expanding that bet comes at the expense of anyone who might be remotely negatively affected by AI. That trend has been in place for some time, but really seems to have solidified into a strategy that is gaining momentum, rather than losing momentum.

So, I guess I hope the correlation holds (even if it seems weird), with both sectors going higher, but for now, I’d be more comfortable betting on alternative managers.

Iran

The ceasefire continues to hold. Iran continues to “negotiate” but offers little. The U.S. military capacity is reaching an apex. The blockade is hurting Iran. The blockade is hurting the rest of the world. The UAE dropped out of OPEC, likely encouraged by the admin, which won’t have much impact today, but sets the stage for a new order of energy dominance. Presumably, Venezuela could also drop out, making the U.S. a deciding factor in global energy prices.

We had yet another Friday, where the market rallied on hopes of a deal, yet, as of now, nothing really new has materialized.

We covered much of this in more detail in Iran and Oil and our April ATW.

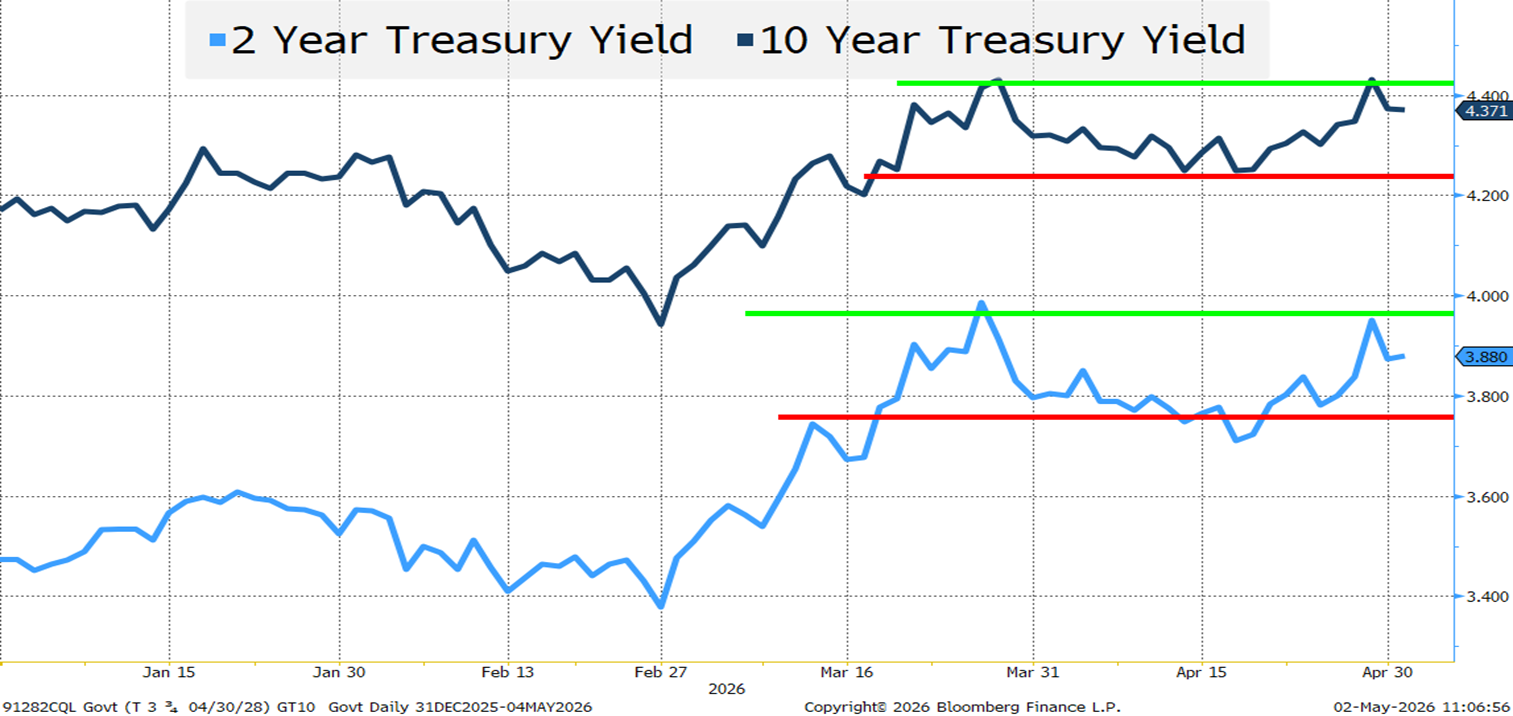

Bond Yields

Treasury yields continue to trade within a relatively narrow range.

Oil is clearly having an impact on yields. As oil prices in “higher for longer,” we see yields inch higher. Anytime the prospect of a deal causes oil prices to decline out the curve, we see Treasury yields respond by drifting lower. How much lower can yields go if we get a deal?

- Does a deal let the Fed cut rates quickly? Doubtful.

- Does a deal decrease our spending in the coming months? Doubtful.

- Does a deal increase our tariff revenue? Doubtful. Does it stop the government from having to pay back claims for inappropriate IEEPA tariffs? No.

- Does it mean the world will go back to being “asleep at the switch” on military risks and slow their spending? Doubtful.

So, we should rally if we get a deal, but I suspect we will not break below 4.2% on 10s.

Then we get the jobs data this week.

Last month’s job data seemed “surprisingly” strong. Like really surprising. Like could it be real or will it be revised down by a lot, surprising. We seem to see almost daily announcements of layoffs.

Yet, initial jobless claims were at like their lowest ever! Given the size of the workforce, that is an incredible feat!

So, do we get another strong jobs report?

If we lived in a world where the price of oil wasn’t having so much influence, the jobs data would be the primary focus this week. By a lot. It will ultimately be a key driver.

- With strong jobs data, look for cuts to be taken off the table and 10s to break out higher, possibly getting to 4.5%. The possibility of a strong week of jobs data is real. The Big Beautiful Bill is helping. ProSec™ is helping. Data center build out is helping (while the data centers themselves don’t do much for employment, the building of data centers helps). Given the drawdown in U.S. energy reserves, it seems clear we are selling more energy products with the Strait closed, which should also translate into jobs. I am leaning towards strong data pushing yields higher.

- While leaning towards strong jobs data, a big revision and miss would not be very surprising. I continue to see problems in data collection (low survey response rates and the birth/death model in a GIG economy), and seasonal adjustments that may not reflect the nature of where business is done in the U.S. relative to where it used to be done.

Mildly bearish on Treasuries here. Only mildly, because we could get a deal, and the jobs data could be weak. But, I think the reaction function to “good” data will be low, while the reaction function to “bad” data will be high. The risk/reward is skewed towards yields not only heading back to the high end of the recent range, but also breaking out of the range to the upside.

Bottom Line

We are living in an AI world. For now, that seems to be benefitting the semiconductor industry the most. Though that is an industry, that in the past, has managed to ramp up capacity to its own detriment. So far, there are no signs of that happening as investment into things that need chips is not only incredibly strong, but it is also showing signs of growing rather than slowing. How long can that continue?

Does current market structure increase the risk that what goes up parabolically, comes down just as fast?

That leaves me roughly where we were last week. Mildly cautious risk, with overweight positions in ProSec™ companies, especially in Europe. Europe probably hasn’t quite “gotten the joke” but they seem to be on the verge of understanding their need to move in the direction of Production for Security, and markets are already placing bets that they will get there.

For those of you not familiar with this theme, this is a report we did to kick of the year – ProSec™ 2026.”

Hopefully, we get a deal, but I’m in the camp that expects one more round of U.S. attacks being required to push Iran to the negotiating table with serious intent to get a deal, rather than Iran just stalling for time, hoping the U.S. resolve wanes, and we “go home” without having largely eliminated the future threat of Iran.