Iran and Compute Credit

The On Again, Off Again War with Iran

Academy’s Geopolitical Intelligence Group weighed in on the Renewed Strikes on Iran.

Brent crude has responded by rising around 10% this week, from a low of $70.14 last Thursday to over $80 yesterday (trading around $79 right now). WTI has been a bit better behaved, but only on the margin.

A lot of algos must still be linking bonds to oil prices, as the 2-year Treasury moved 11 bps higher from Monday to yesterday’s close (it is trading a bit better this morning). The 10-year Treasury had a similar move, which makes even less sense to me.

Yes, my view that we can get to rate cuts as early as September (and will definitely get a cut before a hike) is somewhat dependent on seeing inflation come in lower. Yes, the lifting of restrictions on Iranian oil and better flow through the Strait would help that, so the escalation is a setback on that front. But likely only a minor setback.

While bonds seemed to move tick for tick with oil, stocks were busy doing their own thing.

Stocks, rightfully so, are treating oil as only one of many factors driving prices. Relatively a minor one at that.

The big driver for stocks and some credit spreads is (and will continue to be) the AI spend.

Although ProSec™ was the main theme of the 2nd half of the year kick-off T-Report on Sunday, we also discussed OpenAI, Meta, and Apple.

How Much Will Be Spent on AI? How Will It Be Funded?

Off and on, for the past year, there have been some concerns about how the AI (and data center) spend would be funded. It has been more of a hypothetical debate than anything, as the credit markets had almost insatiable appetite for debt of all shapes and forms (Academy’s Stav Gaon has published multiple pieces on the structured finance side of the AI/Data Center funding).

Amazon brought a mega-bond deal to the market on Tuesday (Academy Securities was a co-manager). The 2046 maturity priced at T+100, only 5 wider than where the 2046 bond priced in March (T+95) (Academy Securities was also a co-manager on that deal).

So, despite some headlines about bond market indigestion on the data center/AI spend, it seems far more “theoretical” than a real issue.

In secondary trading, the market “tried” to take the AMZN bonds wider, but they are now trading in the secondary market around 5 bps tighter across the board versus the spread they came at!

I do believe there is a “cottage industry” of credit “doomers” out there! It was created by the GFC and fueled by the European debt crisis, but it rarely is reflected in the real world of bonds! Many of the issuers in this space have very high credit ratings. Sure, credit ratings have their own set of issues, but we are talking about issuers in the high As or AAs. Supply can weigh on spreads, but the market tends to find a way to make room for bonds that look attractive on a spread or yield basis.

ORCL CDS, which seems to be a favorite topic of conversation whenever anyone is looking at the debt market for this space, is just under 180 bps. Yes, it has been rising for a month, from a low of 155, but it was higher at the end of April and much higher back in March. Most of the purchases of credit protection on ORCL via the CDS market since December of last year have lost money when accounting for carry and roll.

Again, market indigestion or fears might make for interesting conversations, but the reality is that it is easier to make money owning credit than shorting it. Yes, I’m aware that the “path to hell is paved with carry” and will even use that argument when bearish, but carry and roll are your friends in relatively low vol environments (with a few exceptions, VIX has been below 20 since April, and the CDX index has basically been between 50 and 53 since late May).

While so far the bond market hasn’t shown any signs of letting up in terms of issuance, we should see some slowing as it is difficult to see this almost frantic pace of new issue continue! New issuance was not only pushed higher by the AI/Data Center spend, but also by the war in Iran (which, while ratcheting up again, seems more like background noise than a big deal, like it was when it started) and jitters about what the Fed might look like (Warsh has done an excellent job calming those jitters, based on the MOVE index as one example).

Betting against the bond market’s ability to absorb new issue seems like a risky bet here!

There may come a time when we get real indigestion and pushback, but that is not what we are seeing right now. We are mostly seeing posturing, by issuers AND investors, to get the best possible deal for themselves. But the bond market has a “funny” way of getting money day after day (coupons and maturing debt) and that has to get put to work. Much of the market is index based, and those bonds in the indices will find a home.

Some investors, given the size of various issues, may have to get increased credit lines to absorb more, but the combination of ratings and spread likely means those conversations are still occurring, again, supportive for the bond market as a whole and the new issues as well.

What if Spending on Data Centers Slows at All?

The build out phase has had a “the only thing to fear, is fear itself” sort of vibe. The “only” risk was not building as much compute as possible.

Is that still really the case?

- The cost to build compute has gone up. Heck, even memory chips, once viewed quite generically, are very expensive.

- Difficulty getting permission to build compute is increasing. There are plenty of areas still aggressively pursuing compute-related projects, but the NIMBY crowd is growing.

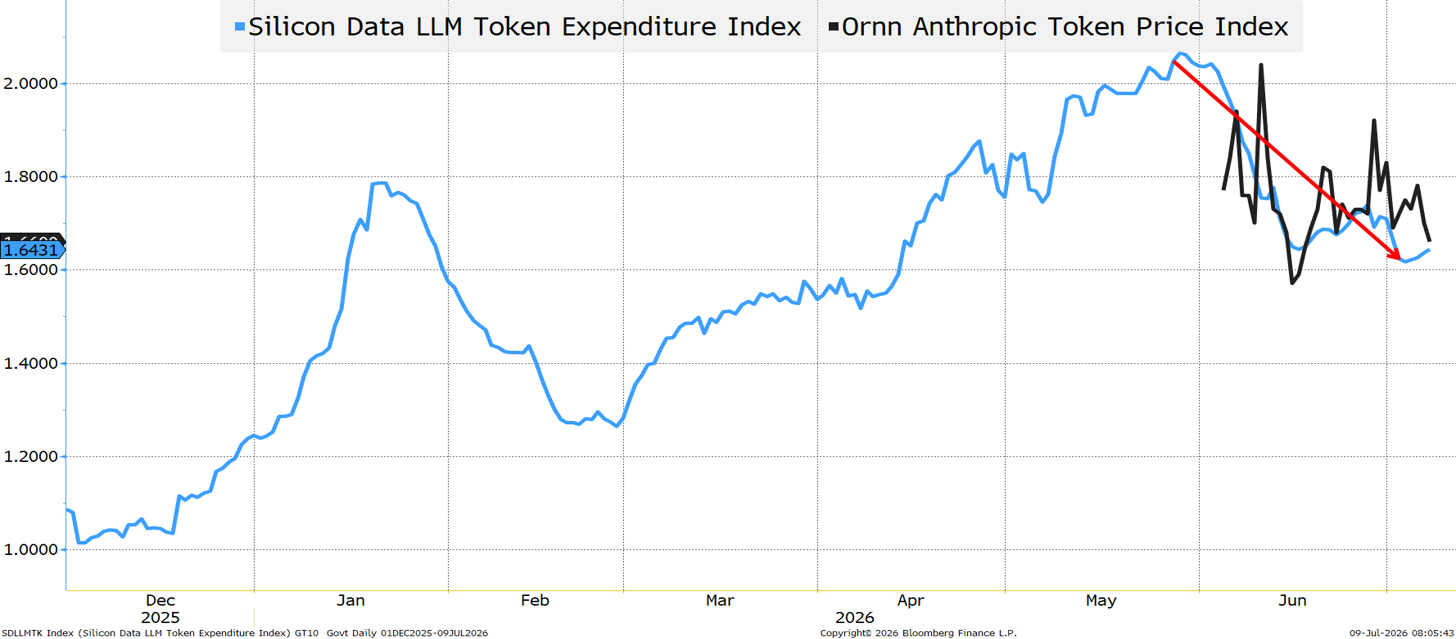

- I am not sure how useful some of the token “indices” are, which makes it extra dangerous to reference, let alone make decisions on, but that’s where I’m at.

If these charts are accurate, spend on tokens has declined of late (everyone experimented with tokens and is now analyzing the costs vs benefits, rather than just being encouraged to spend the most on tokens). Expenditure (and prices paid for tokens) is declining even as costs to grow are increasing? That might be a temporary blip, but it also wouldn’t be the first time markets and companies got ahead of themselves – fiber, everyone needed a “China” plan (some worked, but many would have been better off without a “China” plan), and I’m old enough to remember the Metaverse and “on-line” properties being worth more than some Bored Ape NFTs.

Any sense that spending might slow in the space would be great for bonds (not necessarily stocks, though a Debt Diet can help stocks in some cases as well).

Bottom Line

Credit is still financing revenue, not valuation.

Credit, on the tech side, can be risky when it is funding a technology and really is taking technology risk. For the companies currently coming to market, that doesn’t seem to be the case. Creditors (away from project finance) are funding well-established companies with diversified revenue streams – of which the compute build is just one potential source of revenue.

Credit, especially the “compute” bonds, can drift tighter from here. Even a whiff that spend will come down (either cost to build compute drops as new technologies become available, or companies decide to scale back a bit to make sure their original plans still make sense) would drive markets tighter.

Away from that, I want to own credit in the ProSec™ industries – there will be money raised to fund acquisitions and growth, but the ability to increase cash flow and profits will also be there!