Academy Sustainable Finance Report – February 2026

Key Takeaways

- Power availability, not capital, is emerging as the binding constraint on AI infrastructure growth.

- Local opposition is becoming a measurable execution risk.

- Nuclear expansion offers limited near-term relief.

- Governance and community engagement frameworks may become competitive advantages.

Considering concerns surrounding the impact of AI and data centers to the grid and energy costs, as well as local pushback related to the environmental impact (like noise and water) and property values, we investigate in this update the potential ideal locations (and suboptimal ones) for future AI/data center-related investment. We also look at nuclear generation capacity in the U.S., and which states have shown historically shorter lead times.

We conclude with lessons learned and possible strategies that can be used to help meet demands needed for artificial intelligence and technology at large, while managing a growing state and local resistance. The information is meant to help inform where data center installation can occur with the least friction, leading to more immediate returns.

Power & Pushback

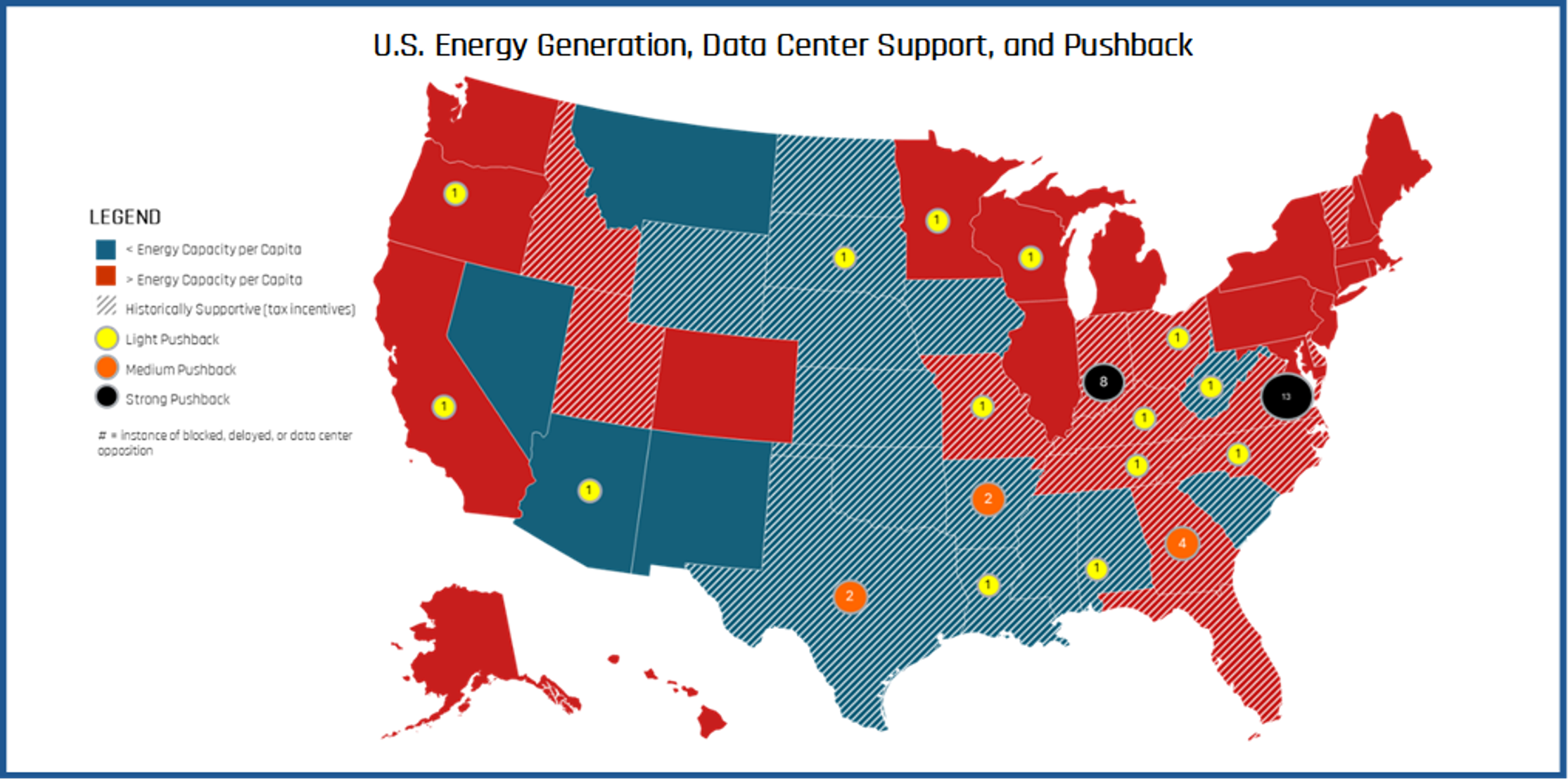

One of the key requirements for data centers, in addition to space, and robust telecommunications connectivity, is access to reliable power (and grid interconnections). Using the U.S. Generator report we were able to break down total generation capacity state by state, on a per-capita basis. At first glance we found 18 states came in above average on per-capita energy generation, mostly in the mid-west and southern U.S. In theory these would be good places to start exploring (sans any water concerns). Most of these states also offer (or have historically offered) some form of incentives/subsidies for data center development.

However, when we examined data center resistance, we found examples of states “richer” in energy and historically supportive, now demonstrating local pushback. For instance, last year there was a 125% increase in data center opposition, affecting over $90 billion in investment.

We found there were 19 states that have shown clear evidence of data centers being either delayed, blocked, or facing potential future opposition.

There is also real risk to existing historical support, as lawmakers reconsider the value of incentives, versus the impact a data center might have on rising energy costs, and infrastructure. This could lead to withdrawals of plans by companies, and increased costs as they relocate data centers from one area to another.

Two other points we’d recommend looking at as well would be water and fiber/connectivity access. Water is a focus in the sense of both access to it, and exposure to wetlands (as data centers will be hard-pressed to build near them). These factors would narrow the aperture significantly. Ultimately, none of this is to say that a data center can’t be built in an area facing resistance, but the headwinds, either energy or regulatory. will be much stronger, and weigh more heavily on returns, versus other potential site locations. Lastly, improvements in technology could be a wildcard. More energy efficient, as well as compact technology, could reduce space, noise, and mitigate energy costs that would assuage concerns and facilitate deployment.

The Nuclear Option

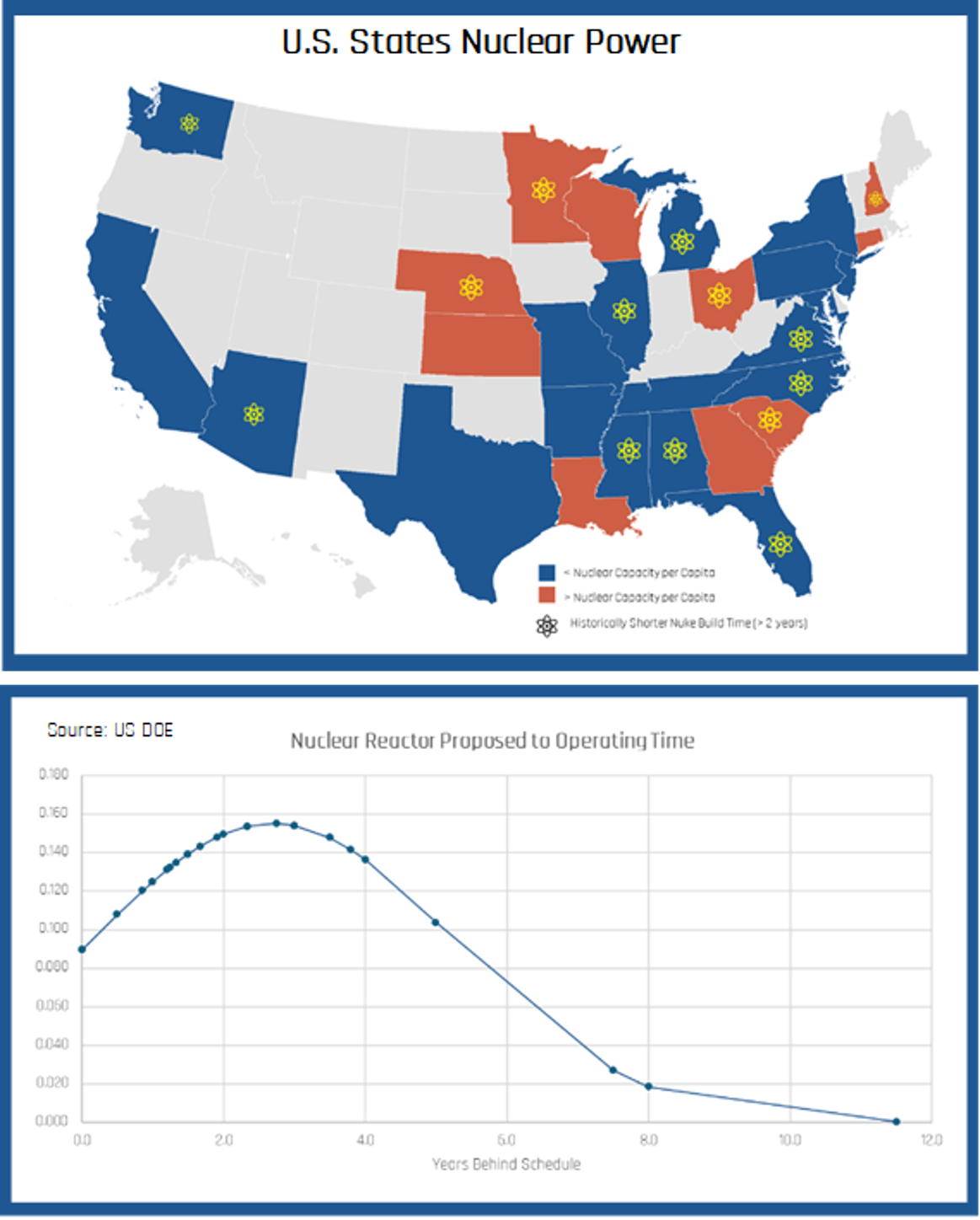

With increasing energy needs, nuclear energy has been floated as an option. Currently, there is only one new nuclear generator planned in the U.S. with the DOE and is expected to be online in 2030. Given the discussion, we wanted to examine how long it took for nuclear generators to become operational, and if there are regions where timelines are reduced.

With increasing energy needs, nuclear energy has been floated as an option. Currently, there is only one new nuclear generator planned in the U.S. with the DOE and is expected to be online in 2030. Given the discussion, we wanted to examine how long it took for nuclear generators to become operational, and if there are regions where timelines are reduced.

After reviewing the generators report, we found on average for nuclear generators that there was 2.7 years in-between the time a nuclear project was proposed and finally operating. Of the 28 states that have operating nuclear generators, 14 of them were able to have nuclear power up and running in less than 2 years. Alabama, Mississippi, and Minnesota had some of the shortest times, while Tennessee, Texas, and Connecticut had some of the longest.

While the 2.7-year average may seem like a short lead time relative to today, it is important to note that most of the U.S. nuclear generator portfolio is over 40 years old, and was either proposed, or under construction prior to the Three Mile Island incident in 1979.

There’s also been discussion and movement in developing more Small Modular Reactors, and while there are currently none operating in the United States, the DOE has allocated $900mm to Genn III+ SMR deployment, and as recently as this month demonstrated the portability of the technology, after transporting a SMR (sans nuclear fuel) from California to an airbase in Utah.

FPIC Frameworks & Data Centers

As we noted previously, stakeholder opposition to data centers has grown. For example, at the end of 1H 2025, there were 17 states with active opposition groups. During this time, opposition and community groups were successful in blocking or delaying 66% of the protested projects. Developments like these underscore the issue that future projects may require an increased emphasis on communities in which operations are occurring, an understanding of local concerns, and how they could potentially be addressed.

One option to initiate this engagement would be for data centers and hyperscalers to establish processes for Free Prior Informed Consent (FPIC). Common in mining and industrial sectors, as well as for sustainable sourcing, FPIC frameworks layout how corporations interact, often with indigenous people when there are plans to develop on ancestral, historic, or sensitive lands. In the process, well in advance of development, relevant stakeholders are informed on the key points of the project, like the nature of the project, its size, pace, reversibility, duration, and rationale. There is no coercion, and the process is directed by those affected (hence free), while participation and consultation remain core components.

It is interesting to consider that FPIC frameworks, often associated with ancestral lands, both domestically, and throughout a lot of emerging markets, would be something that data centers and hyperscalers should consider. It does makes sense when you consider the amount of land being used (in some cases), and the potential impact to energy costs. Should stakeholder opposition to data center development continue, it would be prudent for investors to consider how it is being addressed throughout their portfolio and if processes are in place, like an FPIC framework, that could reduce the likelihood of canceled or delayed projects.

Moving forward, future Infrastructure deployment success will increasingly depend on regulatory and community execution alongside capital investment.

References: Bloomberg, Department of Energy, Data Center Watch, Reuters, American Edge Project, Library of Congress