Academy Sustainable Finance Report – December 2025

2025 saw a unique shift in sustainable finance, where themes like “energy transition” and “decarbonization” have taken a back seat to “energy security” and “strategic autonomy.” Investments that were in some cases subject to exclusion, like nuclear and mineral extraction (especially for critical minerals/rare earths), are becoming more acceptable as institutions adapt to rising costs of energy, and geostrategic risk.

Energy, Data Centers, and Artificial Intelligence Take Center Stage

There continues to be a philosophical shift from energy transition to energy security, which is being driven less by concerns surrounding decarbonization, and instead by domestic production for national security and the increasing demand placed on grids by both data centers and other end-users. Given the growing geopolitical risks, there’s also been a renewed emphasis on defense production and the 5% NATO defense spending mandate (with cybersecurity and AI governance becoming key areas of interest).

There continues to be a philosophical shift from energy transition to energy security, which is being driven less by concerns surrounding decarbonization, and instead by domestic production for national security and the increasing demand placed on grids by both data centers and other end-users. Given the growing geopolitical risks, there’s also been a renewed emphasis on defense production and the 5% NATO defense spending mandate (with cybersecurity and AI governance becoming key areas of interest).

Given the growing demand and policy shifts, the IEA in their Annual World Energy Outlook has adjusted their policy scenarios to now include oil and natural gas growth continuing into 2050, with coal use flattening by the end of the decade. Advanced manufacturing, air conditioning, electrified heating, data centers, and electric mobility are some of the key driving factors, combined with an underinvestment in grid spending. For instance, investment in global power generation has grown 70% since 2015 to $1 trillion a year, while annual grid investment is only $400 billion.

The impact is tangible. Rate payers across all sectors in the United States have had their cost per kilowatt hour go up 5.2% year-to-date vs. 2% last year, with the transport sector seeing the highest increase (8.6%). Residential users are somewhat insulated, with only a 4.9% increase year-to-date. However, when compared to 2015, they have seen their rates go up 36%.

Building grid resiliency, interconnections, and generation capacity is going to be critical in helping control these costs as well as meeting the needs of the 106+ GW in data center power demand expected between now and 2035 — something analysts anticipate costing $200 billion a year in CapEx. The U.S. DoE’s monthly generator report is now forecasting 263 GW worth of capacity to come online between now and 2039. As it stands, that would equate to a little over 20% of planned generation capacity for the United States to be used to power data centers/AI.

Power Purchase Agreements and Framework Finance

One potential option to accelerate capital investment and development of generation capacity is the power purchase agreement (PPA). This is a long-used tool to help off-takers lock in more stable energy pricing and deploy generation. They can be either physical or virtual, with about 60% of the global PPA market utilizing Virtual Power Purchase Agreements (VPPAs).

Through the PPA, an off-taker agrees to buy power from a developer/utility, helping to secure the loan for the developer to build generation capacity (often renewable). Depending on the PPA, energy can be delivered to the site/operations, or virtually, via scheduled settlement and review of the strike vs. market price of energy.

The off-taker also receives the Renewable Energy Credits (RECs) which can range from $1-$60 per MWh, and be as high as $200+ per MWh in some states. Corporations, U.S. tech companies, and hyperscalers are some of the largest players in the space. In 2024, 33% of the 42 GW in annual renewable energy capacity additions were from corporate PPAs and commercial green power tariffs. This year, in addition to some large solar PPAs, we saw a host of nuclear announcements. Large cap U.S. tech companies this year disclosed PPAs to build out nuclear capacity in Illinois, as well as in Pennsylvania with small modular reactors, to power operations.

The off-taker also receives the Renewable Energy Credits (RECs) which can range from $1-$60 per MWh, and be as high as $200+ per MWh in some states. Corporations, U.S. tech companies, and hyperscalers are some of the largest players in the space. In 2024, 33% of the 42 GW in annual renewable energy capacity additions were from corporate PPAs and commercial green power tariffs. This year, in addition to some large solar PPAs, we saw a host of nuclear announcements. Large cap U.S. tech companies this year disclosed PPAs to build out nuclear capacity in Illinois, as well as in Pennsylvania with small modular reactors, to power operations.

To help secure the PPAs, green and sustainability bonds might be a potential option. In previous years we’ve seen issuers come to market, and use proceeds raised to allocate towards PPAs and renewable energy portfolios.

Defense Bonds—Supporting Strategic Autonomy

One of the most interesting developments of 2025 was the formation of the “Euro Defense Bond Label” out of Euronext. 2025 saw two bond issuances totaling 1.75 billion Euro using the “defense bond label” which is designed to enhance transparency, while supporting the EU’s strategic autonomy and resilience by facilitating financing of critical defense and security capabilities.

The label’s eligibility for issuers is primarily restricted to institutions headquartered in Europe, or those incurring more than 50% of revenue, CapEx, OpEx, or payroll within the region. Examples of eligible uses of proceeds include R&D of defense systems, dual-use technologies, surveillance, protection of critical infrastructure, military logistics, and cybersecurity to name a few. Reporting, while encouraged, does not seem to be required.

This tracks with what we have discussed in previous deliverables over the years about integrating cybersecurity, and now AI governance, in framework finance. With threat actors now aided by generative AI, and in some cases governments (which usually nullifies any payment by insurers for a breach), corporate deterrence should be top-of-mind. We see corporate green and sustainability bond frameworks as a tool where issuers can bolt on cyber-use proceeds by raising capital that can be invested to not only enhance energy security, but also governance, through deterrence, site hardening, and cybersecurity.

Sustainable Finance and Investment

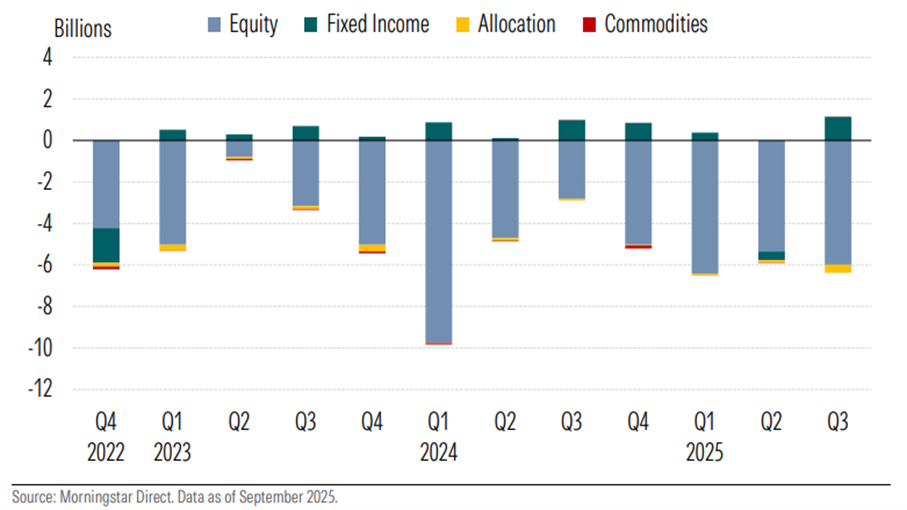

U.S. sustainable open-ended funds and ETFs saw net outflows throughout the year, with actively managed funds accounting for most of the withdrawals. However, investment in sustainable fixed income funds saw inflows, both in Q1 and Q3 2025.

U.S. sustainable open-ended funds and ETFs saw net outflows throughout the year, with actively managed funds accounting for most of the withdrawals. However, investment in sustainable fixed income funds saw inflows, both in Q1 and Q3 2025.

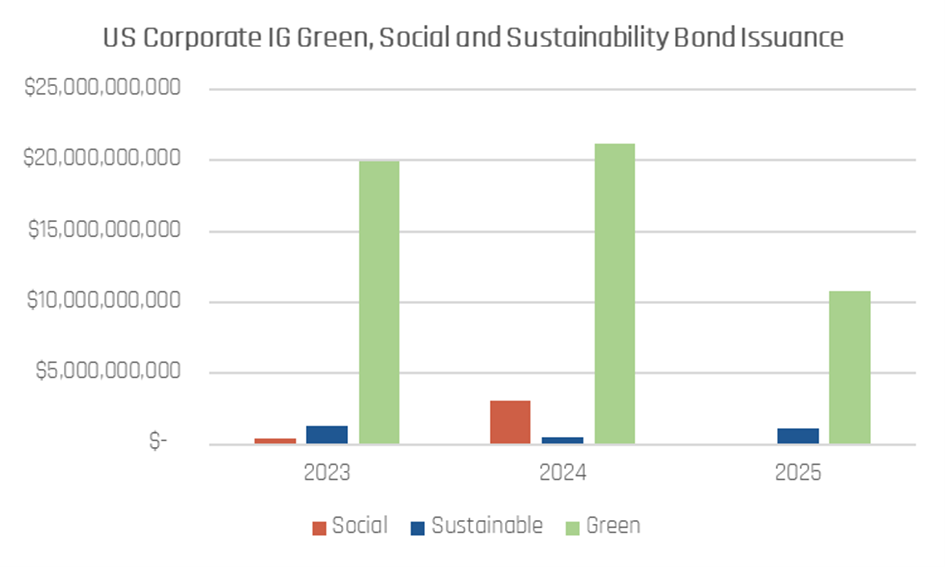

U.S. IG green, social, and sustainability bond issuance remained subdued relative to previous years, with $11.98 billion in IG GSS-labeled debt issued this year. About half of that volume was issued in EUR by U.S. companies. While book subscriptions on average for green bonds were higher, pricing advantages have diminished with green bond new issue concessions averaging 2.25bps versus 2.3bps for vanilla bonds.

Venture capital investment continues into climate tech related areas with Europe leading the way. However, in contrast to previous years, this year, venture capital has been predominantly focused on infrastructure, with alignment in the data center/AI energy nexus, critical minerals, and nuclear. For instance, advanced nuclear development saw $700 million in VC investment, and India’s parliament just recently approved legislation loosening their civil power sector to include private corporations.

Have a great new year and start to 2026!

Further Resources:

IEA World Energy Outlook: https://iea.blob.core.windows.net/assets/dfe5daf4-dbc1-4533-abeb-fafb1faee0f9/WorldEnergyOutlook2025.pdf

Euronext Defense Label: https://www.euronext.com/en/listing/bonds/bond-types/european-defence-bonds

Climate Tech Venture Capital: https://www.ctvc.co/tag/newsletter/