Trade Balances

My Twitter “for you” stream was filled with three themes today:

- A dog who “stole” the Olympics by running with cross country skiers. 😊

- Headline after headline about this being the “most bullish” time ever for Bitcoin. Or, equivalently, some very high price targets (with $1 million not being uncommon). They were treating all of these claims as though somehow the “predictions” are new and interesting, but they all come from the same people who have been making those claims for years. Yawn. The price action (despite widespread support for the industry from this admin) continues to scream “stay away for now” to me.

- That we had a 78% reduction in the trade deficit and the claim that it will go positive this year. I’ve been on the road, so it’s quite possible I missed something. The amount of “bickering” in the comment section, which seemed “insane” even by Twitter levels of “insanity,” also attracted my attention. The back and forth on this seemed insane, as all it would take is about 10 minutes to pull up some data and check this out.

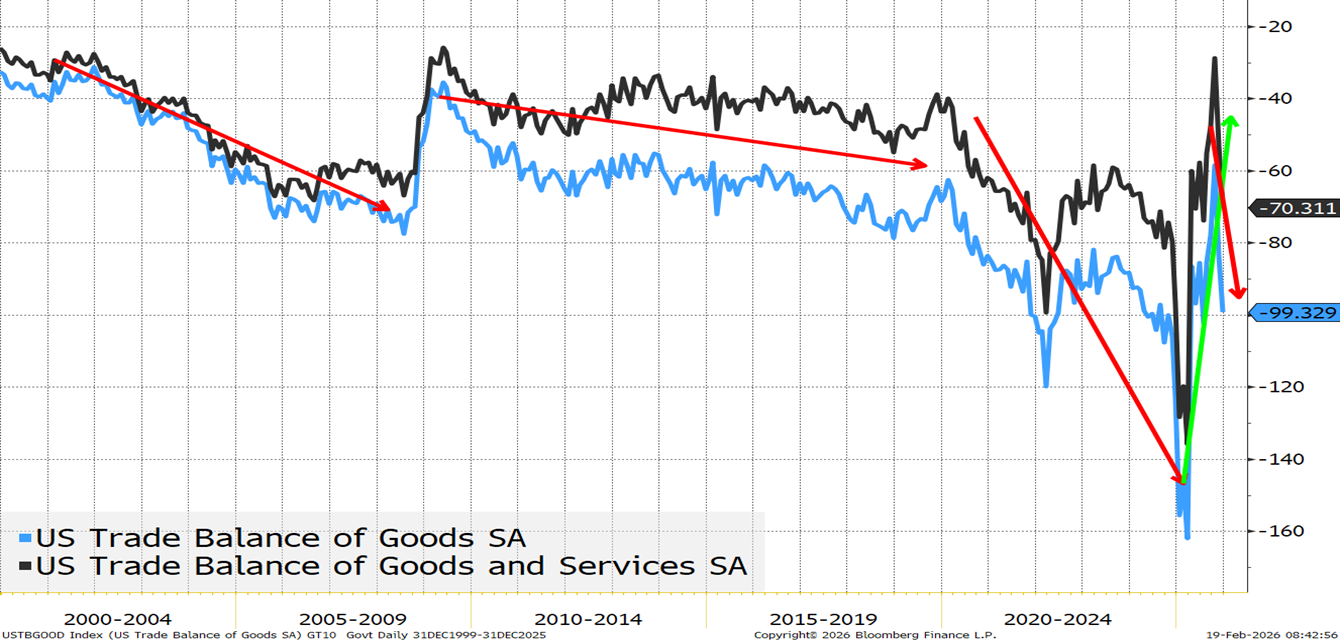

Some Long-Term Trends

Let’s start by taking a longer-term look.

There are three things worth pointing out:

- Trade deficits have existed this entire century. Trade deficits have been with us for some time, but they clearly grew during the early 2000’s (the rise of China). They abated post-GFC (presumably less spending). Trade deficits actually got slightly worse during Trump 1.0 and got a lot worse under Biden (though COVID played a big factor too).

- There is some level of volatility on a monthly basis and annual basis.

- The trade balance on Goods only is worse than Goods AND Services! The U.S. exports services to the globe. We have argued since day one that there has been too much of a focus on trade balances of goods (that may be changing, but the admin was very clearly focused on goods, not the totality of trade).

- I do not know how to calculate this, but I suspect if we had a “profitability” based trade calculation it would look a LOT better for the U.S. (the U.S. imports low profit margin stuff and sells high profit margin stuff). That is clearly the case with services, and likely the case with goods too.

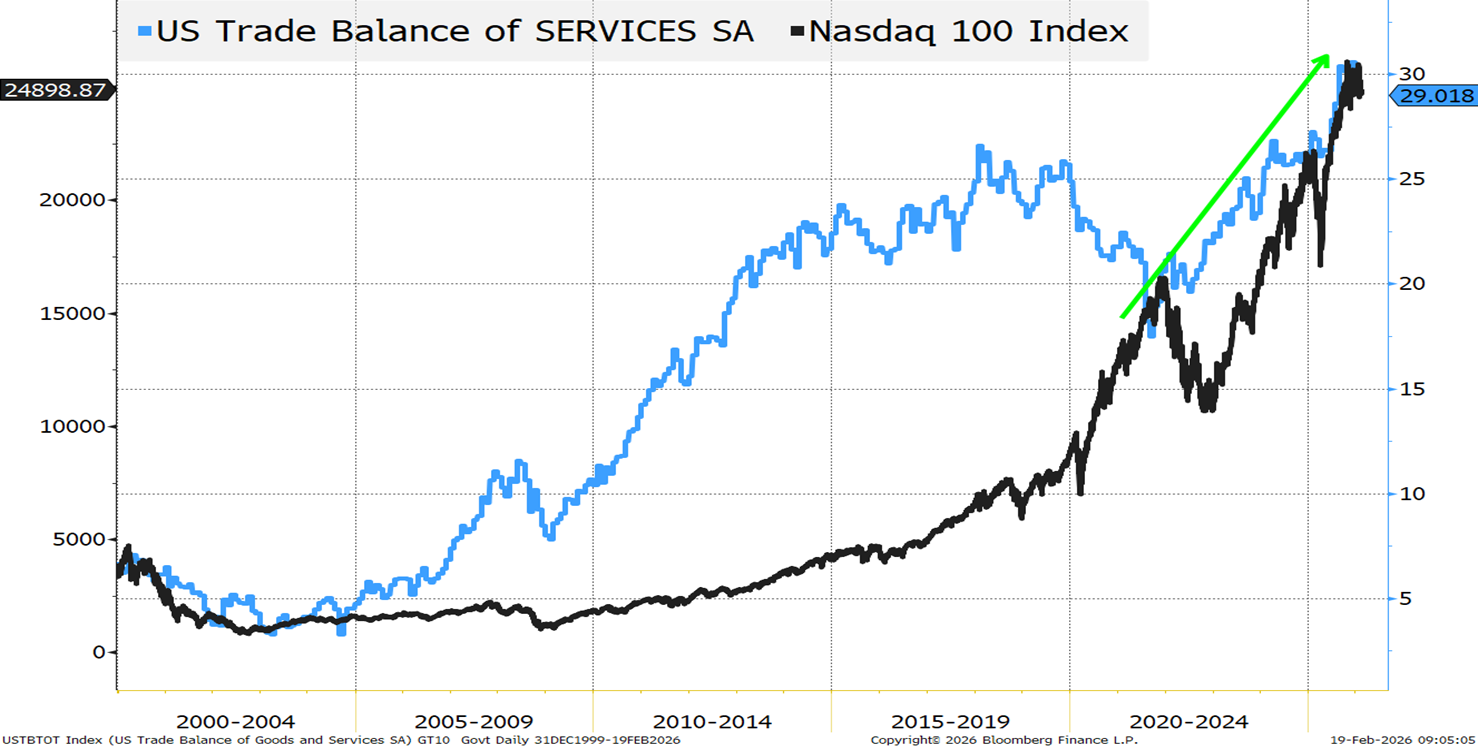

Services Surpluses and the Nasdaq 100

Not the greatest chart in the world, but interesting. It shows trade surpluses in Services and some hint of correlation between Service exports and the stock market.

Service exports (presumably the cloud, data centers, AI, online meetings, etc.) have surged since COVID and the Nasdaq 100 has followed suit. I “only” mention this as we discussed France directing French Government Agencies to use only European software/data providers starting in 2027 (A Bridge Too Far?). While I’m not sure what can be done about it, there was a great deal of angst expressed during European meetings earlier this week about the lack of a strong European competitor in the AI/LLM field at the moment. Policies that encourage Europe to focus on that may be detrimental to U.S. stocks (and service exports over time). Not sure that it is realistic, but it is something that hit our radar screen.

The 78% Decline Is True (kind of)

It’s not that the comment sections that I referred to earlier had an incredibly Orwellian feel (especially the lack of any evidence by either side), but it is what compelled me to pull this together (conveniently on the day we released the data for December).

We often talk about:

- There are three kinds of lies: lies, damned lies, and statistics.

- The Devil can cite Scripture for his purposes.

We try to avoid doing things that fit those two quotations (using different timeframes for different charts to hide or exaggerate things, using different scales, etc.). Having said that, it probably happens from time to time, as constructing and supporting a compelling narrative doesn’t always exactly fit the data seamlessly (otherwise it probably wouldn’t be a compelling narrative; it would be a “given”).

Anyways…

We went with a different time horizon here (see point above) because it makes the following things easier to see.

- The 78% decline in the trade deficit calculation:

- The worst month for the Goods and Services balance was March 2025, just ahead of Liberation Day and in the “heat” of the ramp-up on tariff rhetoric and actual tariffs (Fentanyl-linked ones for example). The Trade deficit in March 2025 was -$136 billion.

- The best month was October 2025 at -$29 billion.

- The reduction was $107 billion ($136 – $29). The change divided by the total is 78% ($107/$136).

- That is the 78% calculation.

- If this “methodology” was applied to the Goods trade balance (which did seem to be the focus until recently, and that change to really include Services in the admin’s thinking is positive) there was a 64% reduction.

- The improvement and overall level in October is one of the best in years. That is a fact.

But the “methodology” makes zero sense.

- The months leading up to Liberation Day were some of the worst trade deficits ever seen as companies ordered goods to get ahead of the tariffs. Those months were worse, in direct response to moves by companies to mitigate the tariff impacts they would feel.

- To a lesser extent, October is typically at the lower-end of the range annually (presumably something to do with when items are purchased for the holiday sales season?).

- In the last 9 months (excluding the 3 months leading up to Liberation Day) the cumulative deficit is $517 billion. On a “straight” average, that would give an “annualized” trade deficit of $690 billion. I was going to argue that we could use the really good month of $29 billion (especially if we are going to go positive) for the annualization, but with November and December both “reverting,” that seems like a stretch.

- The same 9 months (April until December) had a $704 billion deficit. So, on a 9 month vs. 9 month basis, there is substantial improvement (but did the “front-running” reduce imports later in the year?).

- For the full 2024 vs. 2025 comparison, it is $901 billion versus $967 billion. Or a 6.8% decline (not bad, but not 78%). If we go to goods only, the decline is only 4.8%.

- I guess you could have looked at the chart from March 2024 to October 2025 and done a “trend line” showing that we were heading for positive months, but that certainly doesn’t look likely after the November and December data.

We are now approaching the 1-year mark on tariffs and almost nonstop negotiations with countries on tariffs and trade. We have not yet seen whether the “bridge too far” (which focused on Greenland and the Gordie Howe bridge) will impact trade, as it is too recent.

Trade, tariffs, reshoring, and even ProSec™ were always going to take months and years to play out. We are seeing some positives, but there are risks to the strategy and I think those risks have increased in the past month (despite some wild successes like Venezuela).

I remain cautious on risk here.

It is “mildly” strange that I’m a bit nervous sending this piece out, despite the fact that I think it’s both objective and tied to facts? (Other than maybe my perception of Bitcoin in my Twitter feed – which could just be a vibe, rather than fact).