The Fog of War and Markets

Markets often deal with their own version of “the fog of war.” We don’t know the economic data ahead of time. We don’t know what earnings will be (though apparently the industry still does an “amazing” job of generally underestimating them by just enough that stocks can bounce). We definitely don’t know what corporate leaders will say on their conference calls – though there tends to be some consistency over time.

On the other hand, we have a LOT of tools at our disposal to analyze the things we want to predict in advance. From alternative data sources, to “channel checks,” to lending data, to borrowing data, to FedSpeak (which we’ve either been mercifully light on of late, or it is just largely irrelevant until a new Chair takes over). The list goes on.

Contrast that to the conflict in the Middle East.

U.S. troops and equipment. We (market participants) have a rough idea of who is there, what munitions are available, and even potential strategies. The Pentagon and Department of War know the exact status of all of these issues and the actual strategic options being analyzed. “We” should not know every detail, as our enemy would then also know every detail. It is a bit “weird” for Wall Street to accept a lack of disclosure, but that lack of disclosure makes perfect sense. I think we can safely say those leading the U.S. efforts in the conflict have “perfect” information on our capabilities and options.

- Iran does not “know.” Do they see the ceasefire as an opportunity being provided to them because the U.S. wants a deal and knows they need time to organize (which seems to be the latest public rationale for an extension)? Or do they think maybe the U.S. is concerned about weapons stockpiles? About any loss of life in this conflict? About the price of oil, LNG, diesel, fertilizer, and the problems associated with affordability in the U.S. and across the globe?

Iran’s military. There is likely some range of “opinions” on what Iran can bring to bear. While the U.S. government certainly knows better than “us” (the market), it will be difficult to ascertain with any degree of certainty what Iran has left. We likely had a very good idea of “what they had.” A very good idea of “where they make stuff.” Intelligence leading up to this operation seemed incredible. But as the Geopolitical Intelligence Group will tell you, it is difficult to assess damage without the ability to “inspect” it. Satellite images and spy planes, etc., can give us a very good assessment on visual targets. The targets underneath the ground? In hardened facilities? Where presumably the Iranians had some idea of U.S. capabilities and took efforts to protect themselves (and their equipment and production facilities) against what they could expect in terms of attack. Are we worried they have more than is being publicly messaged? Is that the reason for ceasefires? Or do we think we probably don’t “know” for certain that they pose so little of a threat, so the ceasefire is the best means of accomplishing our goals?

Leadership and Decision Makers. From the U.S. side, it is quite clear that the President is the sole decision maker. It would probably be a lot easier for markets if Congress was involved, as Congress is more “predictable” and we’d probably have a lot more comments that we could piece together to form a more consistent narrative. With the President, the market seems to have to lurch from potential strategy to potential strategy. Is the admin being reactive? Or is it playing nth dimensional chess? If it is nth dimensional chess, we won’t really know until after it has played out.

- It is unclear what leadership structure is in place in Iran. Who can make what decision and whether that decision will stand the test of time (we’re thinking the “test of time” is hours and days, not months and years). How do they communicate? Presumably, they remain terrified of being identified and eliminated by the U.S./Israeli intelligence community. Sure, they have taken steps to secure communications, but they probably thought the communications (and before that, the pagers) were “secure” and they failed. How do you coordinate anything in that environment? Is the “Supreme Leader” even alive? Or if alive, does he have the capacity to lead and control anything?

The Strait of Hormuz. Both sides seem to be limiting traffic. Iran tried to control the Strait initially (with a degree of success). The U.S. is over a week into blockading the transit of ships to and from Iranian ports. The U.S. is not positioned to stop ships in the Strait, but to exercise control in regions more conducive to U.S. naval power. This is important as there have been some battling headlines about ships passing through the Strait, seemingly in defiance of the blockade, only to be interdicted in the region the U.S. is comfortably in control of.

- How quickly can the Iranian economy collapse, and does that force them to the table? The U.S. seems to be using the ceasefire as a chance to replenish and restore our fighting capacity (maintenance, new troops, more weapons) while the blockade is intended to bring Iran to the table due to economic destruction. In a “normal” economy, that might not take very long. But Iran is far from a “normal” economy. While not always on a wartime footing, it certainly prioritized the military and the fight against the “great Satan” above overall economic welfare. They are certainly a wartime economy at this point. Russia, the attacker, has been on a wartime economy for over 3 years. Yes, they sell oil (which the blockade is slowing/stopping for Iran), but they are still there chugging along. Ukraine, while being attacked has managed to do enough on a war footing to continue to fight back (increasingly, it seems, with their own drones and weapons being made by Ukraine). In America, we live in a world where the price of gasoline at the pump is going to create angst – fueled by the media. Our tolerance is limited (which seems to be the Iranian bet). An oppressed people in a time of war may not have much choice but to accept absolute misery. Also, who knows how much Iran has stashed away, with IOUs with China, Russia, North Korea, or possibly even in crypto? They did mention getting paid in crypto when getting bribed for safe passage. The U.S. can estimate some of this, but cannot know for certain. It is extremely difficult to not apply some of your own beliefs when analyzing an enemy and underestimating Iranian willingness (and preparedness) for dealing with a dying economy.

One Last Attack. Is this lull just a ploy to prepare for one more round of big attacks to truly wipe out the remaining threat (military and commercial) from Iran? Certainly, many of Academy’s Geopolitical Intelligence Group places a high probability on executing another round of attacks to push the regime into collapse. Does Iran have enough in reserve to cause damage to energy infrastructure in the region so that this would be viewed as a pyrrhic victory? In the battle of wills, intelligence, and command and control, this has to be part of the calculus.

- If it was a game of risk, where all the pieces are known, and it came down to some cards and the luck of the dice, it might be an easy decision one way or the other. With so many unknowns and tensions running so high, it is extremely difficult to be confident on what either side thinks is the best solution. How does the U.S. go from proclamations of “getting the nuclear dust” last Friday to not sending a team this week? Was the proclamation based on discussions with a group in Iran that might not have the authority we thought? If so, time makes a lot of sense for the U.S. If it was another “maximum leverage” ploy, then it might have a bit of “the boy who cried wolf” and be viewed as a sign within Iran’s team that the U.S. is not as strong as Iran feared.

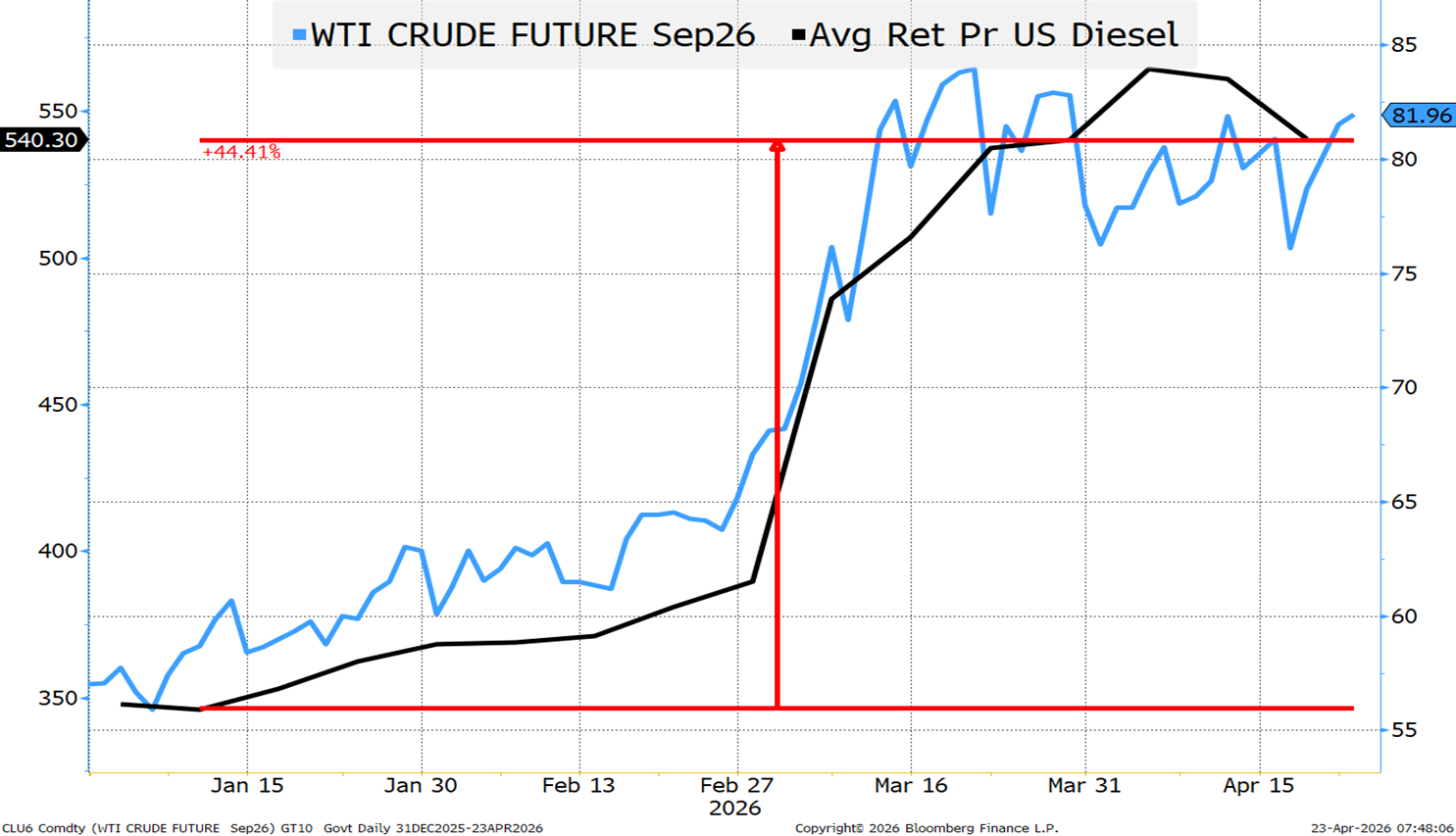

Two Charts

I commit some “chart crime” on this one, but it seemed to be the easiest way to get a couple of points across.

The light blue line is the September WTI contract. For all of the “we are isolated” talk, this is pushing back towards its highs when the front end contract was spiking. While $83 per barrel isn’t shockingly high, it does not bode particularly well for gas at the pump coming into the midterms. It is also heading in the wrong direction since the blockade began. While stocks have almost completely ignored oil and Iran of late, this might be problematic. We have seen some European food retailers discuss higher prices, in no small part because of this conflict. Hence, the desire to highlight diesel at the pump (the chart crime is spot diesel vs September futures and using two scales, neither of which nullify the chart, just things I try not to do). Diesel is up 44%. Farm equipment and the agricultural transportation system rely heavily on diesel. This is going to hit long before the cost of fertilizer (also an issue) hits the price of food. Affordability remains a key concern.

Efficient Markets?

Sure, we can argue that this became a “meme” stock and yes things can happen at the individual stock level that are not completely applicable at the broad index level. But is “not completely applicable” the same as “not applicable at all”? Maybe, maybe not, but it gives me some concern when you can find several examples of this type of behavior (BIRD also comes to mind) and think there isn’t any chance that broad markets got ahead of themselves.

Bottom Line

Anything can happen in Iran still.

My “best case” is that the chatter from late last week of an impending and very strong deal for the U.S. comes to fruition. Still a possibility given the leadership situation in Iran.

The next “best case” incorporating all the work of the Geopolitical Intelligence Group would be another round of attacks that truly topples the regime as we know it. That the combination of military losses and economic problems creates the change that allows Iran to become “normalized” and not a threat to the region. Interestingly, markets may not even sell off much, if the perception is the next attack will be successful in a short period of time.

Other “cases,” include prolonged conflict, to exiting with a “deal” that lets Iran flex power in the region, to something where the “fog of war” lifts to reveal a situation not as favorable to the U.S. as markets are currently pricing in.

In the meantime, we get earnings, where at least that veil will be lifted, for a few weeks, until the conversation shifts to the next earnings season. 😊

So far, we are seeing some large moves (greater than 5%) in some important stocks – in both directions. It will be interesting to see how the software story, the AI/Data Center story, and the consumer story unfold as earnings come out, all with Iran as a backdrop.

I’m more comfortable with high quality fixed income than either rates or risky credit here. But I’m more comfortable with them than stocks. On stocks, I continue to believe in the Global ProSec™ theme where companies that are vital to creating Vertically Integrated Nations do well!