Hey Mate, The Genius of Mariah Carey, and More

Having just returned from London where we watched consensus for a “Santa” rally grow, it seemed like a good time to discuss a couple of things:

- Things we didn’t know we needed, but apparently, we did.

- Biggest differences between our London and U.S. geopolitical/macro meetings.

We will address positioning, consensus, and I daresay, overbought conditions early in the week, as we recover from jet lag, but for today, these “concepts” are top of mind.

The Genius of Mariah Carey

Who knew that the world desperately needed a new Christmas song? Apparently Mariah Carey did when she released “All I Want For Christmas Is You” back in 1994 (I have to admit, I didn’t realize that it had been around for so long). This song now appears at or near the top of every single holiday playlist, and according to AI (which I believe in this case), it has generated more income for her than anything else she has written.

So what else is there in terms of things that we didn’t think we needed, but maybe we do? Let’s start with BITCOIN.

Bitcoin broke $100,000 last week. Despite a plunge of 10% in a matter of minutes (wild ride), it managed to reclaim $100k and is trading right around that level as we write this T-Report. I’m highly confident that by the time you read this report it will be somewhere between $90k and $110k (which is a pretty wide range, almost laughable, yet the sort of range we all are forced to accept when we get the monthly jobs data foisted on us – see A Tale of Two Reports).

The move in Bitcoin is largely understandable (so far) and I wouldn’t fight it, yet. President-elect Trump and his crypto entourage (entourage feels more appropriate than administration when looking at crypto) are clearly going to provide more clarity (and ease of access) around crypto than it was getting of late (despite approvals of “spot” ETFs, etc.). His team has a lot of people really fixated on crypto and it certainly seems as though that community put a lot of money into the election (however, not for the first time as SBF, in particular, seemed to have been a major contributor during the prior election).

There is chatter about the U.S. holding on to the Bitcoin it already has (mostly captured, “shockingly,” through raids on criminals). Typically, the U.S. sells these holdings over time, but there is a big push for the government to hold them. That at least makes some sense to me, as behavior around “free” or “found” money tends to be different than money that is earned (one main explanation for all the luxury stores in Vegas).

There is a loud and vocal group (everything about crypto tends to be loud and vocal) that wants the government to buy Bitcoin. Effectively issue debt and buy Bitcoin. The assumption (or presumption, or just wild fantasy) is that the increased value of Bitcoin down the road will pay off that debt. You could argue that it is being done on a personal level and maybe even on a corporate level, so why not at the government level? I completely disagree with this concept.

- The future price of any asset, let alone one with a lot of digital ones and zeroes, is not certain – despite what the crypto hype will currently tell you. I’d much rather have seen the U.S. buy stocks years ago. They at least have a long track record of working over time and generally supporting the U.S. economy. I don’t see this with crypto (despite Bitcoin having had an incredibly strong annual and decade-long performance). The fact that I’m even compelled to write this opening sentence is bizarre, but it seems necessary (or maybe I just spent too much time on Twitter while on the road). Even the complete rug pull of the HAWK “meme coin” has done little to shake the conviction of many that crypto and the meme coins are the easiest path to becoming rich (going forward).

- Despite Trump sending a “you are welcome” congratulatory social media post to the crypto community when bitcoin crossed $100k for the first time, I find it difficult to believe his love affair with crypto will last. He likes “control” and by definition no one controls crypto. However, the reality is different – from just a few holders owning a disproportionately large portion of Bitcoin, to influencers who seem to be allowed to say and do anything to pump the price, it remains the wild west. My first “rule of crypto” remains true – that there are no rules in crypto. The love affair is still in the early stages, and Trump does have loyalty to those who helped fund his campaign, but I don’t see this as a lasting relationship, especially as he will likely get a lot of pressure from the National Security element of D.C. to be cautious on helping crypto too much.

But, for now, it is apparently something that many didn’t think we needed, but maybe we do? I can’t believe it will last, but it is out there and something to discuss at holiday parties!

Speaking of things that I don’t think we need, but apparently we do, just look at MSTX! I do not like the concept of single stock ETFs. Leveraged single stock ETFs, where the returns are path dependent (daily rebalancing requires, at the close, selling on down days and buying on up days to rebalance for the next day). That is a drag over time. But here we are. MSTX has a market cap of $2 billion with an expense ratio of 1.29%! It was only launched in August. So, less than 6 months into its existence, the Defiance Daily Target 2X is on a run rate to generate $25 million per annum! The “beauty” of MSTX, is that it is well known (and quite simple) to run a leveraged ETF and things like NVDL have provided a path for regulatory clearance documentation. NVDL is another single stock ETF, with $6 billion of AUM and a 1.06% expense ratio – on a run rate of over $60 million per annum, at the 1-year mark. Who would have thought that you could create $25 million or more, just by leveraging up a widely held, easily tradable, stock? Not me, but there it is.

While I’m not sure that any of these things point to a “bubble” mentality, I think they start to fit the narrative, especially with the rise of leveraged single stock ETFs, and their story will come up in our positioning and consensus report.

Maybe we all need to think like Mariah and even if others don’t see the need, to go ahead and put it out there?

London

Let’s start this section with a holiday song, too. I knew, as we were going down into the tube station and the GIG members we were with questioned the choice of “Fairytale of New York” (a song played by a busker in hopes of making money), that we had a lot of interesting things to discuss! He literally recognized the Pogues in about 3 beats.

But I digress (kind of) and there are a few key takeaways that came up that are worth mentioning.

- Russia and Ukraine. Consensus even amongst our Geopolitical Intelligence Group members including General (ret.) Sir Nick Parker, who ran security for the London Olympics and Admiral (ret.) Sir George Zambellas, who was also the First Sea Lord, was that the road to peace is far less likely than “we” (the Americans) think. A big part of this, or really the main reason for this, is that Europe is much more afraid of giving anything to Putin than the U.S. seems to be. The immediate extrapolation is that giving Putin anything will lead to him coming back, in very short order, to take more. While the companies and banks we deal with in the U.S. have operations in the region, we don’t often talk to the people directly supervising those areas on or near the borders of countries that Putin could go after next. I’m still digesting the conversation, as a more pessimistic view on the outcome is interesting and plausible, but I’m still in the camp that we see some sort of deal reached. I also think that the “U.S.” narrative on how it could play out helped the conversations, but this was definitely a discussion where the differences were acute.

- The conclusion, if we are correct and there can be a deal early in the Trump administration, is that the companies who are prepared to move quickly and aggressively back into the region have a lot to gain, as many are very nervous.

- Poland is front and center in terms of places to invest. Not just now, but certainly on the back of any peace deal, as they will be an integral part of NATO’s strategy going forward and the nation has really shone during the war! I’m not sure how to invest in Poland, but hands down they have been a “winner” during the conflict and are likely to be an even bigger winner if a deal is reached.

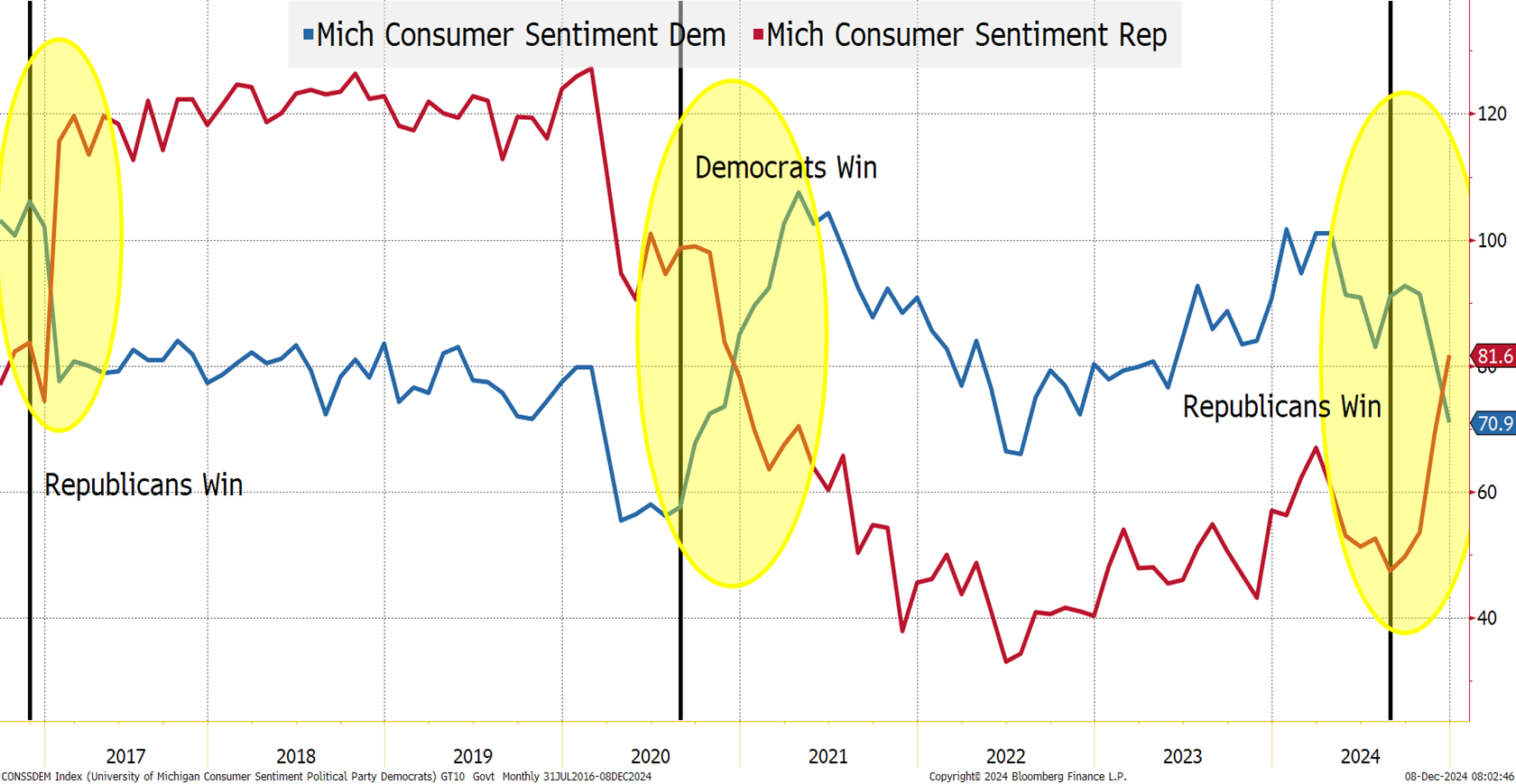

Finding things to like about Trump. As discussed in An Amazing Country, we came across regional differences (and differences by industry) regarding how people were viewing the future. We’ve already pointed out this chart – CONsumer CONfidence by party, where “shockingly” (maybe I spent too much time in the U.K. and am letting my sarcasm take over more than usual) Republicans now have a better outlook on the economy than Democrats.

So, we see some of the concern about President-elect Trump here, but it was more pronounced in Europe.

- When we discuss the possibility that M&A activity will “normalize” under Trump (the FTC won’t waste ammunition on every single case, especially on cases where it is clear from the start that they won’t win), people get genuinely interested. For anyone in banking, a return to a healthy and readily understandable M&A framework will be good for business. It gives corporations a lot more avenues for growth. That argument just didn’t seem to garner the excitement in the U.K. as it does here. Maybe, because much of the business will be in the U.S. and in many cases we weren’t talking to those who would benefit most directly from that business, it was a contrast that is making me think.

- Is the separation of the U.S. and Europe likely? Is there a rift that is widening? I don’t know, and I don’t think so, but I’m certainly thinking more about it. Without a doubt, the Russian invasion of Ukraine has tightened the ties within NATO, at least from a military perspective. But from an economic standpoint, are the relationships fraying? Is the U.S. big enough to “go it alone” versus China? Can Europe “fight” China? Should it? I think so, but that isn’t the vibe there. In recent years, whether it was the European Debt Crisis or Brexit – Germany (and to a large degree France) were pillars of strength for the EU. The German economy was a juggernaut and both countries remained committed to policies that the EU had embraced wholeheartedly (like immigration). The German economy is struggling (basing an economy on cheap energy from a country like Russia and relying on sales into a country like China “might” not have been the best strategy) and politically the environment is changing in both countries.

- Everyone is curious about the D.O.G.E. and what can be accomplished. In response to my “over/under” comment on how long the Trump/Musk relationship will last, one client had a great story. They were at a wedding, where unbeknownst (wow, I did spend too much time in London) to the couple, people were making side bets on whether they would last a year (they didn’t).

A lot to unpack.

Should U.S. stocks be trading at much higher multiples than European stocks? I don’t know and that is especially true given how global many of the companies are, but as much of a contrarian as I am, I’m not sure I’m ready to bet on mean reversion next year. I probably should, and maybe it was just a “vibe” while there, but I didn’t walk away thinking I need to pound the table on European stocks. That could change (and positioning and consensus is so set up for a contrarian), but it isn’t top of mind.

Top of Mind

Trump likes “chaos.” He likes his starting positions in negotiations to be “extreme.” Since consensus has now accepted his current positions as “normal,” look for him to ratchet up his rhetoric to reset the negotiation starting points even further away.

Bottom Line

I do not like Treasury yields here. Friday’s reaction to jobs was too optimistic for cuts and I expect that yields will push higher in the coming weeks. Not much higher (4.4% on 10s would be a buying opportunity), but the squeeze and the overly pessimistic views on inflation prospects have been largely taken out of the market.

Doing more work on the positioning of risk assets, and if crypto and leveraged single stock ETFs are any indication, I’m not going to like my conclusion on what is next for risky assets (even in the sectors that I’ve liked). I was a bit surprised that the S&P 500 is up “only” 1.6% in the past 30 days. With last week’s gain of just under 1% and all the hype and daily “all time high” headlines, I would have thought it was up a lot more than that for the past 30 days (the Nasdaq 100 was up 3.3% last week, but only 3% in the past 30 days).

Maybe, since my work is likely to make me bearish, I’m delaying the work because December is a tough month in which to turn bearish. Seasonality tends to be real and powerful. It also tends to be a month where trends are followed rather than broken, which again points to strength.

One thing that was reinforced both in Europe, but also by the headlines out of South Korea and Syria, is that the world remains volatile and we are in a “weird” position where President-elect Trump seems to be dominating the headlines, but President Biden remains in charge, and specifically is the Commander-in-Chief, which just seems weird to many who are used to very quick turnarounds post- elections.

Looking forward to another interesting week and our annual holiday party, which has grown a lot since I joined the firm, but still includes each of the branches singing their respective songs! The Marines are at a distinct advantage, given their number and how cool any song that starts with “From the Halls of Montezuma” has to be.

For what it is worth, I’m still voting for the Waitresses – “Christmas Wrapping,” as my favourite holiday song. 😊